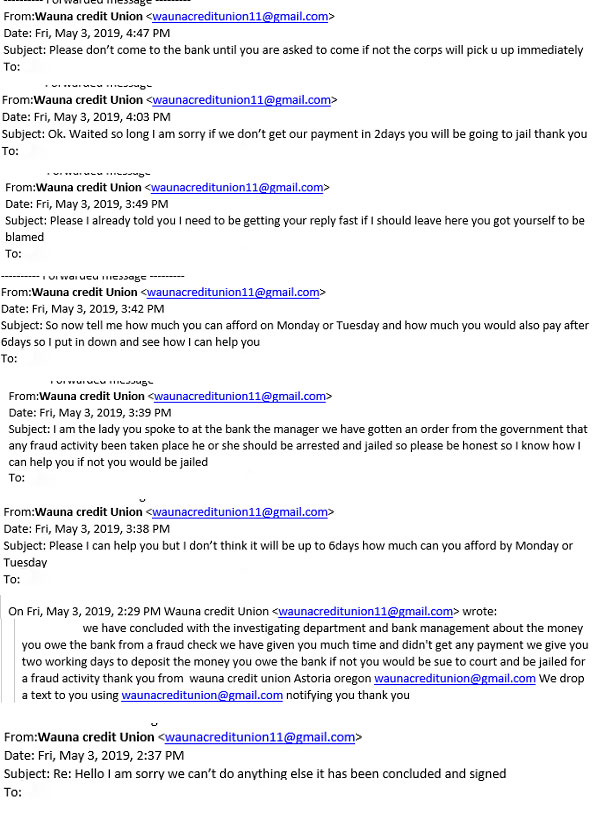

A sad truth is, those who are looking to take advantage of people, or scam the system, will use all tools at their disposal, regardless of how much it hurts others. One of the ways people have been cheating the system since the pandemic started is unemployment fraud. For those who don’t remember our blog post from last May, unemployment fraud is when a scammer uses somebody else’s identity and falsely claims unemployment insurance. In many ways it’s the perfect crime. The government will usually make the first couple of payments before the claim is disputed, and the victim happily has their job, and doesn’t even know somebody has claimed to be them until it’s too late.

How late is too late? For many it’s when they receive a 1099-G and file their taxes. Unemployment income is income, and the IRS expects its cut. So what to do if there’s a 1099-G in your name when there shouldn’t be? The Internal Revenue Service (IRS) recently issued guidance for taxpayers who receive Forms 1099-G for unemployment benefits they did not actually get because of identity theft.

Taxpayers who receive an incorrect Form 1099-G for unemployment benefits they did not receive should contact the issuing state agency to request a revised Form 1099-G showing they did not receive these benefits. Taxpayers who are unable to obtain a timely, corrected form from states should still file an accurate tax return, reporting only the income they received. A corrected Form 1099-G showing zero unemployment benefits in cases of identity theft will help taxpayers avoid being hit with an unexpected federal tax bill for unreported income.

The IRS previously issued guidance requested by states on identity theft guidance regarding unemployment compensation reporting. No Forms 1099-G should be issued to those individuals the states have identified as ID theft victims.

Skimmers are sneaky little devices, which fraudsters affix to ATMs or other machines that accept credit or debit card transactions. The skimmer then secretly swipes your card information whenever you slip your card into the affected machine. These pesky gadgets have been around for years. But thieves are continually improving them and their usage doesn’t seem to stop!

Skimmers are sneaky little devices, which fraudsters affix to ATMs or other machines that accept credit or debit card transactions. The skimmer then secretly swipes your card information whenever you slip your card into the affected machine. These pesky gadgets have been around for years. But thieves are continually improving them and their usage doesn’t seem to stop!

different than what should be expected.

different than what should be expected.