Everybody likes a summer vacation, but travel can be expensive. If you’re looking to squeeze one more getaway into your budget before summer ends, our financial aces here at Wauna Credit Union have some tips for traveling on the cheap and getting the best deals.

Everybody likes a summer vacation, but travel can be expensive. If you’re looking to squeeze one more getaway into your budget before summer ends, our financial aces here at Wauna Credit Union have some tips for traveling on the cheap and getting the best deals.

Go in the Off-Season

During the hottest summer months, business at popular vacation spots like Arizona and New Mexico tends to slow down dramatically. If you can take the heat, you can score some great deals at premium resorts, golf courses, and other attractions during the off-season. Just remember that the off-season is also when many of these places perform annual maintenance and major construction projects. If, for example, a pool is important to you, make sure the resort you’re visiting won’t be renovating it while you’re there.

Buy a Package

When considering a last-minute getaway, travel packages that combine flights, hotel, and sometimes meals, can be the best deals out there. The key is to be flexible on where and when to go.

Get the App for That

These days, there’s a travel app or website for pretty much everything – including the lowest-priced flights, hotels, and travel packages. A few to consider include Kayak, Hipmunk, Momondo, Airfare Watchdog, and Skyscanner. Each has a slightly different focus, so try out several to see which ones work best for your needs. Keep in mind that some of these sites do not carry regional airlines, which often have good deals. And, when you do find a great flight deal, take a look at the airline’s website, since some deals are only available when you book direct.

Get Social

Just as some deals are only available when you book direct, some travel operators offer special deals for those who follow them on social media. The best deals go fast, so follow your favorites on Facebook and Twitter, and subscribe to their promotional email lists. If you live in a smaller town, you could save by driving to a major city where flights are generally cheaper. By the same token, if you live in or are flying to a metropolis like Los Angeles, be sure to look to smaller airports like Burbank, Ontario and Long Beach. They may be slightly less convenient, but many low fare carriers favor these regional airports because their fees are often lower.

Capitalize on the Strong Dollar

If you’ve avoided historically- expensive destinations like Japan, now’s your opportunity to visit and cross them off your bucket list. The strong dollar means exchange rates are favorable, and your money will go farther. If you want to stay closer to home, travel gurus also recommend Canada, since it’s 40% cheaper than it was a year ago.

If you’ve been meaning to talk to your kids about money, April is the perfect time to start. In addition to

If you’ve been meaning to talk to your kids about money, April is the perfect time to start. In addition to  The key difference between local credit unions and other financial services is that we are owned by members like you. Unlike for-profit financial institutions, which take their marching-orders from stockholders, we exist only to serve you and your financial needs. You’re the boss! With no Wall Street fat-cats to pay, we are uniquely positioned to return direct financial benefits to members. This includes better interest rates and lower fees.

The key difference between local credit unions and other financial services is that we are owned by members like you. Unlike for-profit financial institutions, which take their marching-orders from stockholders, we exist only to serve you and your financial needs. You’re the boss! With no Wall Street fat-cats to pay, we are uniquely positioned to return direct financial benefits to members. This includes better interest rates and lower fees. Do you want more examples of the benefits of belonging to a credit union? How does earning a better return on your savings sound? 2018 also saw the collective member benefit from higher interest rates on savings at more than $3.6 million. We supported local spending to the tune of $333 million. Not to mention a $1.8 billion boost to the Oregon economy.

Do you want more examples of the benefits of belonging to a credit union? How does earning a better return on your savings sound? 2018 also saw the collective member benefit from higher interest rates on savings at more than $3.6 million. We supported local spending to the tune of $333 million. Not to mention a $1.8 billion boost to the Oregon economy. So you’ve set a budget and on paper it looks fabulous. You’ve created different spending categories and what seem like reasonable limits. Yet, somehow it just doesn’t quite work month after month. Sound familiar? It’s frustrating, but there are fixes.

So you’ve set a budget and on paper it looks fabulous. You’ve created different spending categories and what seem like reasonable limits. Yet, somehow it just doesn’t quite work month after month. Sound familiar? It’s frustrating, but there are fixes. The solution? Set up recurring transfers from your checking to your savings account through U-Banking. Designate a day (preferably just after you get paid) and a predetermined amount, then let technology do the rest. That way, you’ll always hit your savings goals every month.

The solution? Set up recurring transfers from your checking to your savings account through U-Banking. Designate a day (preferably just after you get paid) and a predetermined amount, then let technology do the rest. That way, you’ll always hit your savings goals every month. Brrrr! For many of us, winter means high energy bills, but sitting in the dark or turning off the heat are not your only options. Here are some ways to improve your home’s energy efficiency and save money during the cold months:

Brrrr! For many of us, winter means high energy bills, but sitting in the dark or turning off the heat are not your only options. Here are some ways to improve your home’s energy efficiency and save money during the cold months:

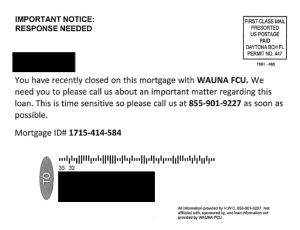

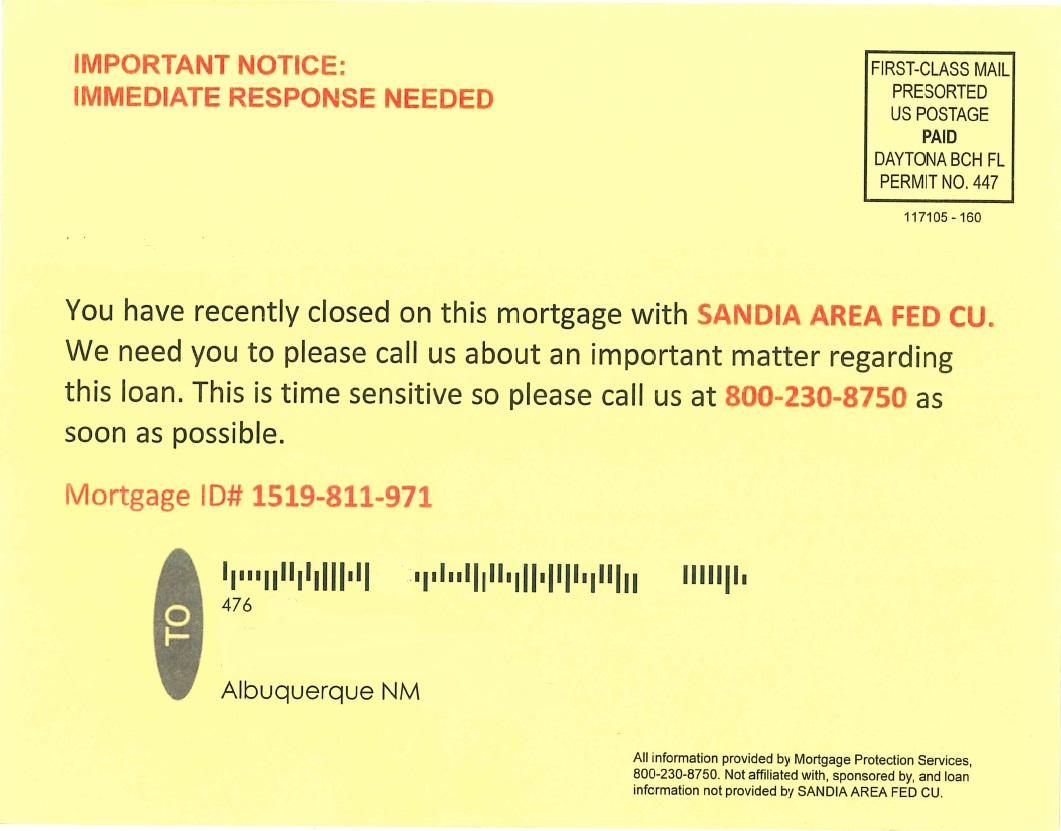

Darn right we called the number. In fact, we tried all the numbers we were able to find. Some connect to a live person, others are recordings, and one dialed directly to an automated system. Regardless of which number, we were eventually probed for personal information. Funny enough, these fraudsters refuse to give out any information about themselves, or even the actual company they are working with.

Darn right we called the number. In fact, we tried all the numbers we were able to find. Some connect to a live person, others are recordings, and one dialed directly to an automated system. Regardless of which number, we were eventually probed for personal information. Funny enough, these fraudsters refuse to give out any information about themselves, or even the actual company they are working with. As your credit union, we want to help you make the most of your time and money during the holidays while keeping your financial information safe and secure. Smart shopping strategies can also keep your finances from going “into the red” on Black Friday.

As your credit union, we want to help you make the most of your time and money during the holidays while keeping your financial information safe and secure. Smart shopping strategies can also keep your finances from going “into the red” on Black Friday. If you’ve ever let a debt go unpaid, your creditor probably sent it to a debt collector. Debt collectors are serious about getting you to pay. That’s why part of their strategy is to list the unpaid account on your credit report. This in turn damages your credit score, and appears on your report for future lenders to see. Your collection will remain on your credit report for up to seven years.

If you’ve ever let a debt go unpaid, your creditor probably sent it to a debt collector. Debt collectors are serious about getting you to pay. That’s why part of their strategy is to list the unpaid account on your credit report. This in turn damages your credit score, and appears on your report for future lenders to see. Your collection will remain on your credit report for up to seven years.